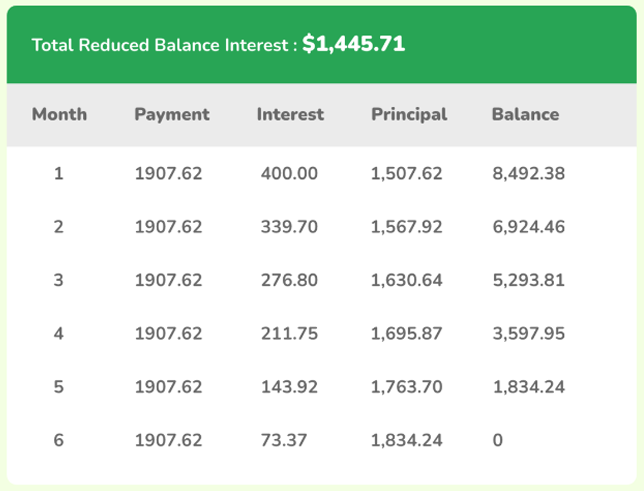

Annual interest rate = 48%

Per month interest rate = 4%

1st month interest calculation:

$10,000 (Outstanding balance) x 4% (Interest rate per month) = $400

2nd month interest calculation:

$8492.38 (Outstanding balance) x 4% (Interest rate per month) = $339.70

3rd month interest calculation:

$6924.46 (Outstanding balance) x 4% (Interest rate per month) = $276.98

4th month interest calculation:

$5293.81 (Outstanding balance) x 4% (Interest rate per month) = $211.75

5th month interest calculation:

$3597.95 (Outstanding balance) x 4% (Interest rate per month) = $143.92

6th month interest calculation:

$1834.24 (Outstanding balance) x 4% (Interest rate per month) = $73.37